Quick pitch: Kronos CVR is too cheap!

Letting Kevin Tang rob me. AGAIN

This will be quick and I will not start at zero here. Kronos (KRON) is a failed biotech company, selling itself to the “liquidator” Kevin Tang represented by Concentra. Deal terms are as follows:

Receive 0.57$ per share via Tender Offer expiring June 13

Receive a CVR with various payouts but one of them being “at least” 0.29$ per CVR (or that´s what it looks like)

You have 0.86$ in “hard value” via cash coming - what is that worth today and is it worth holding out for the remainder of the CVR?

Company expects 61.432 mln CVRs will be outstanding

Spoiler: I think the stock is worth 0.90$ to 0.95$ which means the CVR is worth 245% to 390% of what the market implies at 0.87$ per share

Identifying a valuation floor

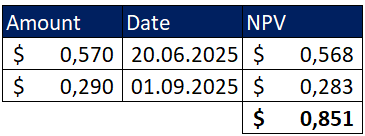

The two payments known are roughly worth 0.851$ per share if you discount by 10%:

With the stock ending yesterday at 0.87$, you are paying just 2 cents more (or 1.22 mln US$) for the following payout possibilities (the above mentioned 0.29$ are “Additional Closing Net Cash Proceeds”):

Just glancing at this for 20 seconds, it becomes quite clear, that solely (iv) will probably cover the current cost of the CVR or at least a substantial portions via the fixed payments.

I could start flabbergasting about the various assets (do not ask me what a p300 KAT inhibitor is or what it´s worth) and their value, but I will leave it at that: Most biotech assets bring in something. I have rather little conviction in payments from (i): 2 years is an invitation to Tang to slow walk the process. (ii) is looking more promising with 6 years. We basically need almost nothing in value here to pay for the CVR (if (iv) doesn´t do the job).

So I guess we can be sure: The CVR looks pretty much like a no brainer. You pay almost nothing and have various ways to win, especially through the fixed payments from (iv). It´s simply a free call option or at least looks like it.

It is also extremely encouraging that the company resolved its lease situation by itself and did not let Kevin Tang do that. It seems trust between the parties only goes so far and that is a very good thing. We might get lucky and receive even more “Additional Closing Net Cash Proceeds”. The former CEO is a large shareholder and seems motivated to maximize his own payout. If shareholders are indeed lucky, the CVR is actually trading at a negative price right now.

The whole process of determining the “Additional Closing Net Cash Proceeds” so far is very obscure, since we have no idea what the “post closing liabilities” are (the basis for the “savings”-calculations).

Where is the risk?

Nothing is ever risk free and while that is already true in bioland, CVRs are their own wild west. I think the risk is pretty low, but it´s not zero. ChatGPT summarizing the terms regarding the “at least 0.29$-payment”:

So Concentra will have 30 days after closing to dispute the “Additional Closing Net Cash”, especially if new claims arise. Kronos is in a wind-down since November 2024, so I think the potential for negative surprises is quite low. But the main risk is sitting probably right here.

I don´t think there can be meaningful dispute with regards to yesterday´s cost savings of 0.29$ per CVR:

The parties have a “net cash schedule”. I guess Tang had 38.7 million US$ in expenses for the lease (lease payments, maintenance, heating, whatnot) in it over the years, all of that got settled for 20.5 million US$ net yesterday and here we are.

Trading the CVR

Obviously this is extremely price sensitive. If you buy the stock at 0.88$ vs 0.87$, you are not paying 1 cent / 1,1% more - you are paying ~3 cents instead of 2 cents for the CVR (if the 0.29$ savings hold) which means 50% more. Only think about what you are paying over 0.851$ as your price paid for the CVR.

Additional thoughts

I think the CVR ist most likely worth 3-6 million US$ (or 0.048 to 0.098 per CVR) in excess of yesterdays 0.29$ per CVR but has some very decent moonshot optionality especially through (ii).

Tang holds very little shares (~2%) himself, so he has every incentive to bullshit CVR holders.

Bischofsberger as a large holder seems aware of this conflict and might be willing to sue (always good to have large holders in a CVR imo).

For some older Tang CVRs I received a somewhat meaningful borrow fee over the years as some holders seem to have been short the stock. Might or might not happen again.

Happy to hear pushback / other pitfalls in the agreement or hints for asset valuations.

This will be the last time Tang screws me. For sure!

Disclaimer: Nothing on this blog is investing or financial advice, do your own DD. I do have a beneficial long position in KRON as of writing.

P.S.: You should check if your tax situation allows a purchase if you choose to do so, you need to be able to effectively net the “stock loss” (you buy stock at 0.86 and sell to Tang at 0.57) against the “CVR gain” (the hopefully 0.29$).

I looked at this a little while back. Has a Kevin Tang CVR ever paid out? His track record spooked me. Interesting though.